Key Takeaways:

- GLP-1 drugs have pioneered obesity medication.

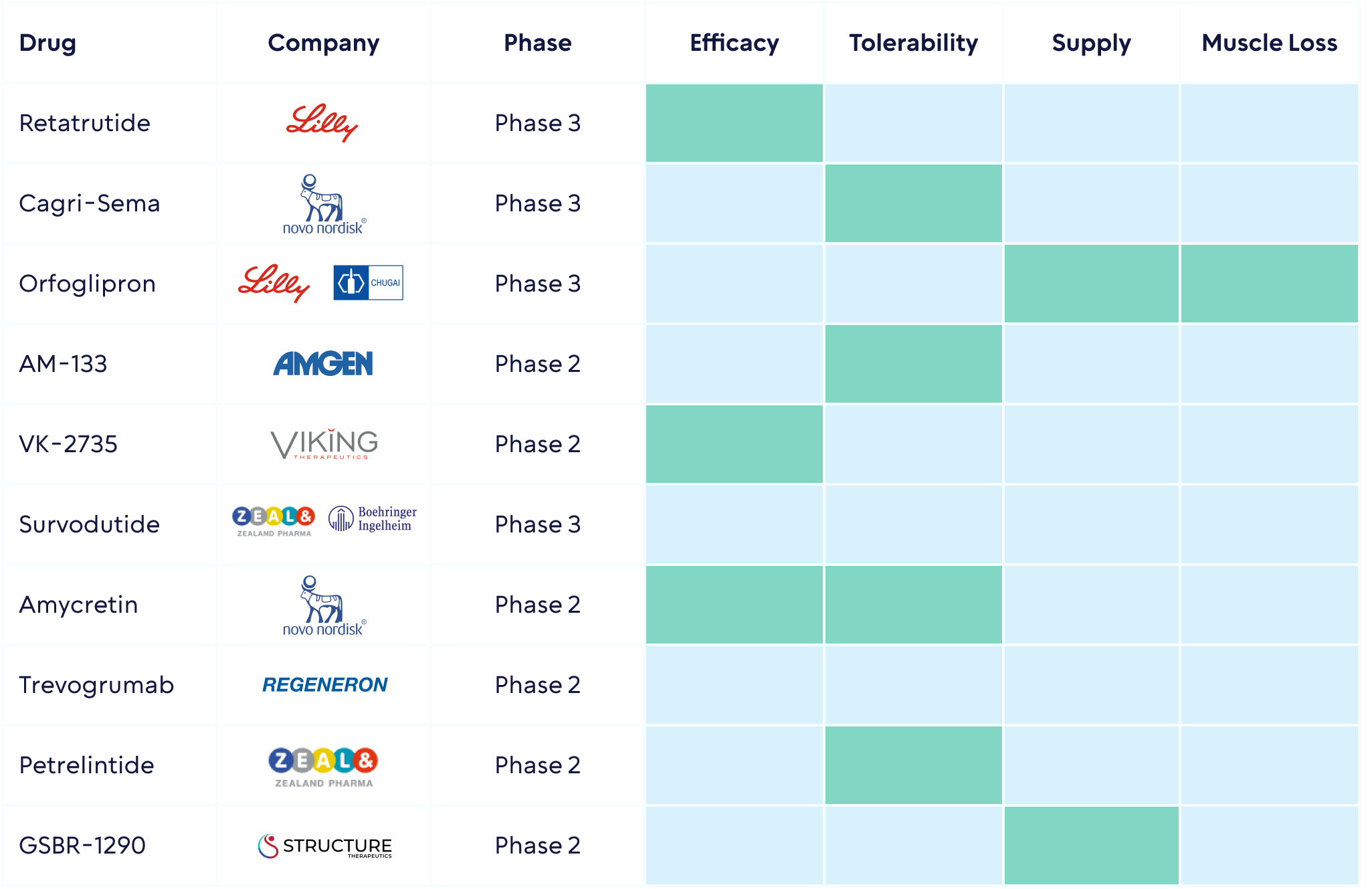

- Yet the race is on for the next generation, and we explore 10 promising new drugs in development.

- These drugs address various issues with GLP-1s including efficacy, tolerability, muscle loss and supply/manufacturing.

- The exploding landscape, by some counts over 330 obesity medications under investigation, requires expertise to navigate.

- One way to gain exposure is through the Tema Obesity & Cardiometabolic ETF (HRTS).

Download the full report in PDF

1. Eli Lilly's "Triple G" GGG - The Most Potent Drug?

Garnering a standing ovation at the American Diabetes Association conference where results were presented, Lilly’s so called “Triple G” is going after efficacy gold. In a mid-stage trial it showed weight loss of up to 24.2% at 48 weeks. Retatrutide targets GLP-1, GIP, and glucagon, three hormones responsible for insulin control and feeling full, hence the triple G nickname. This drug is being tested in weight management, obstructive sleep apnea and knee osteoarthritis in Phase III trials. The key question with this high efficacy will be tolerability, and data so far showed some dose-dependent elevations of heart rate, which bear monitoring.

2. Novo Nordisk's Cagri-Sema – Evergreening The Franchise Part I

Novo Nordisk, the leader in weight loss market, is going after tolerability instead of efficacy with this combination drug targeting GLP-1 and amylin. Phase II data showed 15.6% weight loss at week 32. The theory is that amylin is a lot more tolerable than GLP-1. Novo are so confident in this pipeline asset that they are even running a direct head to head trial against Lilly’s Zepbound.

3. Eli Lilly & Chugai Pharmaceutical's Orforglipron – The Leading Oral

This is non-peptide oral, compared to current injected GLP-1s, which means it is a lot easier to manufacture. The drug achieved on average 14.7% weight reduction at week 36.

4. Amgen's AM-133 - Once A Month Dosing

Amgen are taking a unique approach. They have developed an antibody (a more complex molecule than a peptide) that antagonizes GIP. This means the drug could be a lot longer acting reducing dosing to potentially just once every two months. Amgen argue this could mean much better tolerability. We don’t have much data yet and the Phase I so far was mixed, with Phase II data coming this year.

5. Viking Therapeutics' VK-2735 - The New Kid On The Block

Fresh off the press Viking reported statistically significant weight loss of 13% at 13-weeks, which didn’t show signs of plateauing. The last point means it could be higher as more weeks of data are collected. This is a very competitive profile.

6. Zealand Pharma & Boehringer Ingelheim's Survodutide - Leading In Liver Disease

Survodutide is a peptide targeting GLP-1/GIP. The drug recently showed very promising early Phase II data in MASH, a liver disease closely associated with obesity. 83% of patients saw significant improvement in their diseases compared to 18% on placebo. A statistically significant improvement in fibrosis was also observed. The drug is also being tested in obesity where data is expected potentially next year.

7. Novo Nordisk's Amycretin - Evergreening The Franchise Part II

At their 2024 capital markets day Novo Nordisk announced results for their second follow up to semaglutide – Amycretin. It is a clever combination of GLP-1 and amylin being tested both as a pill and sub-cutaneous injection. The oral drug showed 13% weight loss by week 13, which beats Wegovy at the same time point. 80% of patients at that point were still on the drug, a self-described “impressive” retention rate suggesting very good tolerability.

8. Regeneron's Trevogrumab – muscle sparing

As is the company's DNA Regeneron are going for a completely innovative approach. Their expertise is muscle loss, which their CSO, Dr. George Yancopoulous, called “catastrophic for patients”. Their drug, Trevogrumab, inhibits myostatin, where there is pre-clinical data that shows muscle gain. As an aside and earlier stage, Regeneron are interested in understanding obesity as a heterogeneous disease and, through the Regeneron Genetic Center, finding and developing novel genetic targets for obesity.

9. Zealand Pharma's Petrelintide – more tolerable?

Zealand is also investigating a drug targeting amylin which they think could be used in co-formulation with other peptides including GLP-1. Amylin is seen as a much more tolerable target than GLP-1 with comparable efficacy. An update on the drug will occur in 2Q 2024.

10. Structure Therapeutic's GSBR-1290 - another oral competitor

Another competitor focusing on a white pill for GLP-1 is Structure with their drug GSBR-1290. These drugs could be a lot easier to produce chemically than the current peptides. Early data showed promising efficacy in non-diabetic obese patients comparable to Lilly’s Orforglipron with a downward trend in weight loss, although the effect size was less than that of Orforglipron in diabetes subgroup.

Conclusion

Drug development is a constantly evolving race and carries significant risks from scientific to commercial. No area is this truer than the current race for the next generation obesity medications. Navigating it requires expertise, something inbuilt in the Tema Obesity & Cardiometabolic ETF HRTS.