By clicking below you acknowledge that you are navigating away from temaetfs.com and will be connected to temafunds. Tema Global Limited manages both domains. Please take note of Tema's privacy policy, terms of use, and disclosures that may vary between sites.

Start investing now

Start investing now

Invest directly by choosing one of the brokers below

Start investing now

Invest directly by choosing one of the brokers below

Start investing now

Invest directly by choosing one of the brokers below

Start investing now

Invest directly by choosing one of the brokers below

Start investing now

Invest directly by choosing one of the brokers below

Start investing now

Invest directly by choosing one of the brokers below

Your are leaving temaetfs.com

Which fund are you interested in?

Life Sciences

HRTS

Obesity & Cardiometabolic ETF

CANC

Oncology ETF

MNTL

Neuroscience and Mental Health ETF

Core Equity

TOLL

Monopolies and Oligopolies ETF

RSHO

American Reshoring ETF

Thematic

LUX

Luxury ETF

ROYA

Global Royalties ETF

Why ROYA ETF?

Differentiated commodity exposure

Royalties can provide exposure to the revenue streams of a collection of assets related to commodities such as gold, oil and gas, and base metals

Capital light and scalable

Royalties provide scalable exposure to cash flow streams while mitigating operational and financial risks

Contractual real income

The contractual, inflation-sheltered cash flow stream of a royalty business allows it to pay out competitive and compelling real dividend income

Alternative asset class features

Royalties are typically structured products that provide exposure to unique private assets, like pharmaceutical patents and intellectual property, while minimizing dilution risk

Inflation hedge

Inflationary environments will typically benefit royalty companies as they earn cash flow directly from revenue lines, that benefit from rising prices

Fund Overview

Fund Details

As of May 03, 2024

Primary Exchange

CBOE BZX Exchange

Ticker

ROYA

AuM (USD)

$265,503

# of Holdings

27

Fund Inception Date

08/16/23

Gross Expense Ratio

0.99%

Net Expense Ratio*

0.75%

Implied Liquidity (# of shares)

ETF Implied liquidity is a representation of how many shares can potentially be traded daily in an ETF as portrayed by the creation unit. This is defined as the smallest value of the IDTS (Implied Daily Tradable Shares) for each holding in the creation unit.

273,585

Implied Liquidity (USD)

ETF Implied liquidity is a representation of how many shares can potentially be traded daily in an ETF as portrayed by the creation unit. This is defined as the smallest value of the IDTS (Implied Daily Tradable Shares) for each holding in the creation unit.

$7M

Shares Outstanding

10,000

Investment Advisor

Tema Global Limited

Sub-Investment Advisor

NEOS Investments, LLC

*Contractual expense cap for net expense ratio of 0.75% is in effect through 06/30/2025.

Fund Summary

The actively managed Tema Global Royalties ETF seeks to provide a balance of long-term growth and current income by investing in listed royalty companies that provide structured exposure to revenue streams from commodities, pharmaceutical, entertainment and intellectual property assets. Royalty companies earn a share of future revenues in exchange for investment. Royalties accrue directly from the revenue line of an underlying asset, underscoring their scalability while avoiding most operational and financial risks. As such, these businesses are able to generate contractual real income for investors.

Portfolio Manager

Investment Partner

Chris Semenuk

Chris is a global fund manager with more than 25 years of experience, 20 of which was spent managing a $5 bln global equities fund at TIAA, a leading US based financial services company. Chris managed the fund since inception and raised several billion dollars in assets over that time period. Chris has a Bachelor's Degree in Economics from Union College in New York State.

How does the Tema ROYA ETF fit in a portfolio?

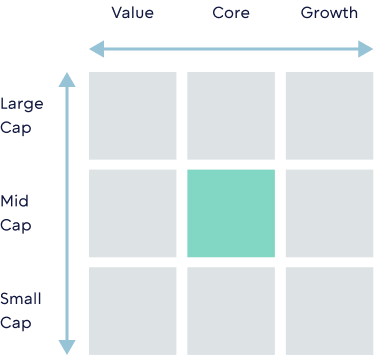

Investment Style Box

Source: Tema. The investment style Box reveal’s a fund’s investment strategy by showing its investment style and market capitalization based on the fund’s portfolio holdings.

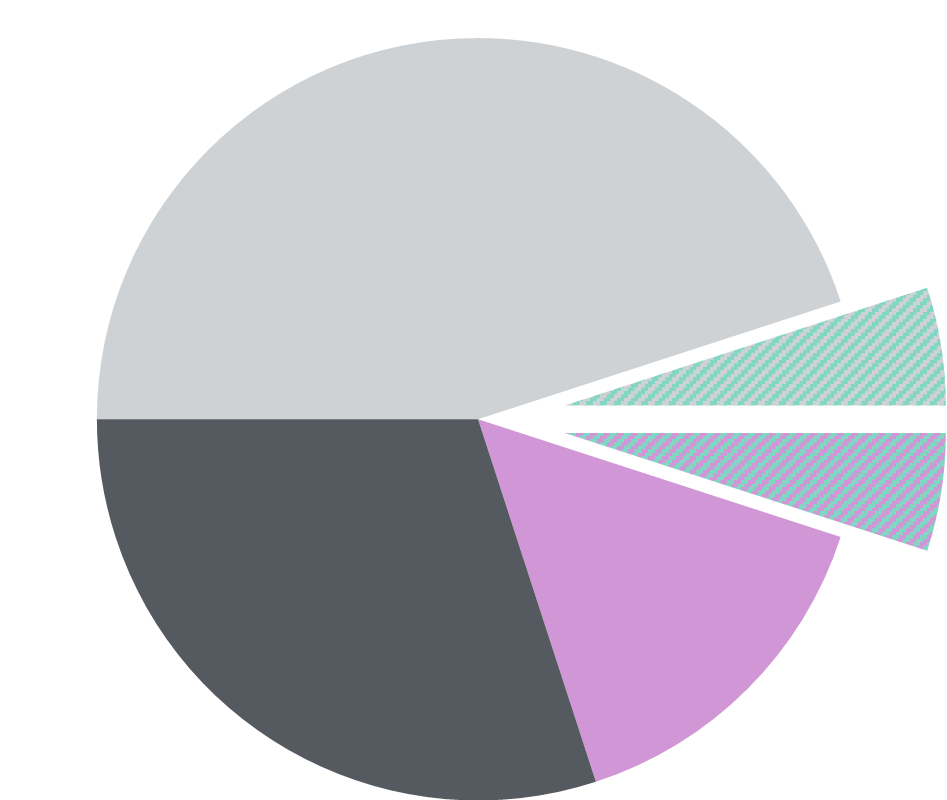

Potential Portfolio

Equity Allocation

5-10%

Equity, Commodities, & Alternatives

ROYA ETF - Equity

ROYA ETF - Alternatives

Equity

Fixed Income

Commodities & Alts

Where could a position be funded from?

- Could be funded from an existing broad market equity exposure.

- Could be funded from a commodities and alternatives exposure.

- May play an income provider role in a portfolio

How to buy

*Neither Tema Global Limited nor undefined ETF are affiliated with these financial services firms. Their listing should not be viewed as a recommendation or endorsement.