Once we establish that the company under analysis has solid foundations and meets pillar one (operating base) and pillar two (balance sheet and cash flow), we can start to assess if the stock is a good investment with a view to the upside. To do this prudently our third test involves building a valuation case.

Valuation can be framed in an almost countless number of ways, and it is important that individual portfolio managers are left to their preferred approach. Our process focusses on coming to a valuation case for every investment we make rather than being prescriptive of how that case is built up.

A flavor of some of the approaches we take to value stocks is presented below.

- Whether a company is trading at a discount to its own historic multiple range, for example a pe ratio one standard deviation or less below the historic through cycle average.

- Cheap compared to the fundamentals of the firm, especially if those are improving and correlated.

- Attractively valued when compared to close peers, especially if there is a business transformation that brings them closer.

- Sum of the parts (SOTP) or hidden value situations.

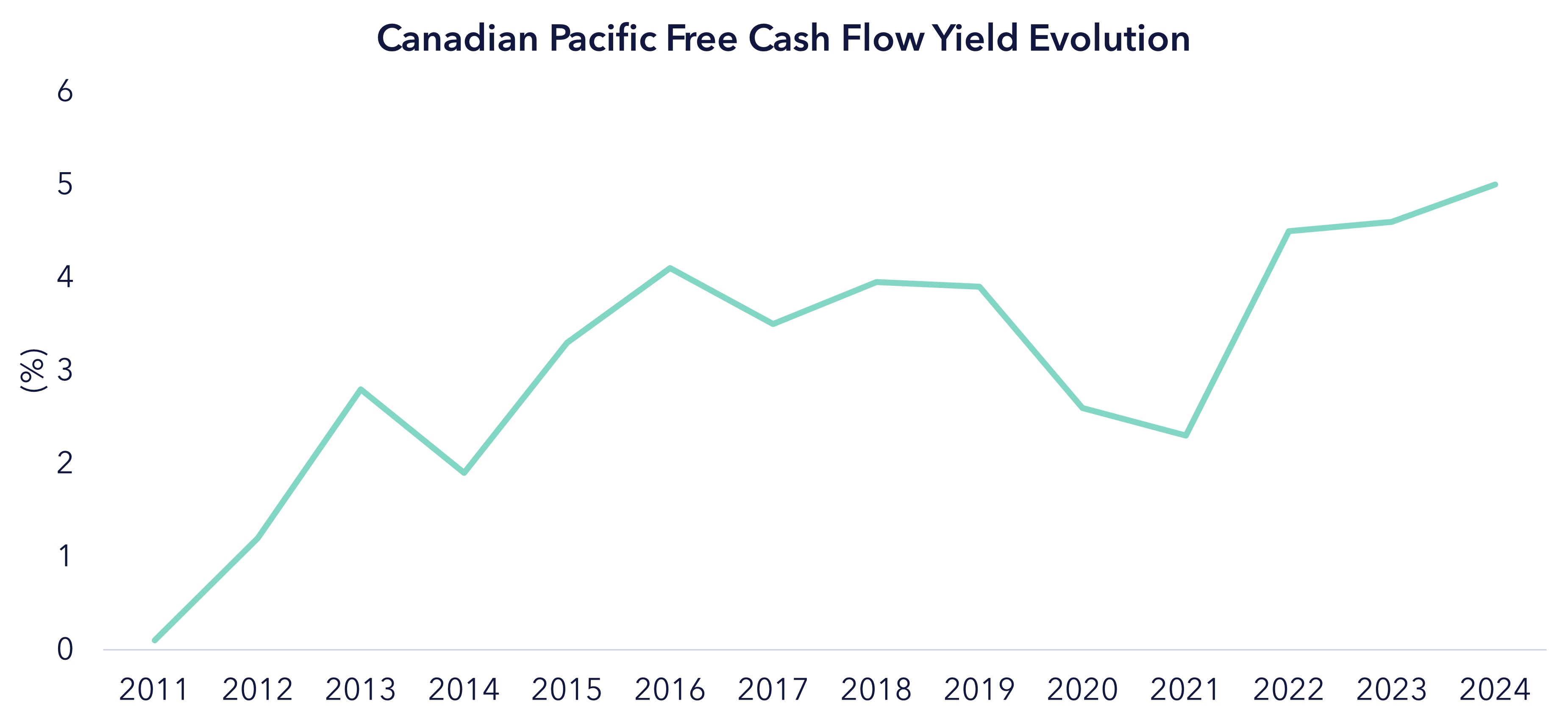

A good example is Canadian Pacific (owned on our TOLL fund). If you looked at the free cash flow yield of the company on the surface 4.6% (at time of acquisition) might not seem attractive. However, relative to the trading history (the average since 2011 was 3.0%) this is actually a very attractive price. This is especially so if one considers the uniqueness of this rail franchise – the first to connect all four corners of North America – and the 15-20% EPS growth management target over the medium term.

Source: Bloomberg

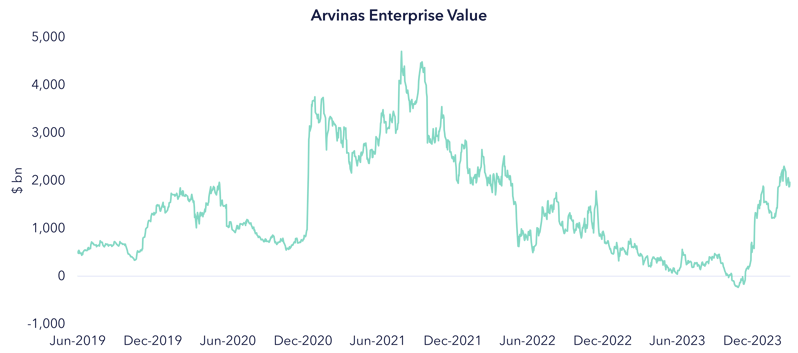

Platform technologies are notoriously difficult to value as these are often pre-revenue with commercialization far in the future. Arvinas is a good example. They pioneered protein degradation technology. Unusually, their technology was validated in multiple targets in areas like breast and prostate cancers. During the biotechnology boom in 2021 this platform was valued as high as $4.5bn in enterprise value. It then traded all the way down to $300m amid a brutal bear market for biotechnology stocks. At this level we felt there was exceptional value for this type of platform and pipeline and included the stock in our launch portfolio for CANC in August 2023.

The shares continued to fall, hitting negative enterprise value, in other words a market cap below the value of cash on the balance sheet. Since then, they have recovered strongly to nearly $2bn in enterprise value on the back of further positive pipeline progress in 2023.

Source: Bloomberg

Another example is Terex, owned in our Reshoring fund. The company is perceived by the market as a maker of scissor lifts under the brand name Genie. Yet 50% of the revenues are from materials processing equipment, think machines used to crush rock. This segment has a strong track record of double-digit sales growth and 18% operating profit compounded annualized growth rate (CAGR) since 2016. Yet despite this the stock trades on 8x forward P/E, or a nearly 50% discount to industrial machinery bellwether CAT.

One explanation could be margins, where CAT consistently makes 18-20% through the cycle. Interestingly, Terex is opening a new manufacturing facility later this year that they believe will get their materials processing margins closer to those of CAT. Layered on top of this the growth coming from reshoring and large US infrastructure projects, we believe makes Terex shares attractively valued.

Conclusion

Our third pillar asks what the valuation case for each security is, leaving freedom for individual fund managers to determine how that case is built.